Table of Contents

Retirement is a dramatic life transition. One of the major changes that occur when you retire is financial: you no longer receive a regular paycheck from your employer. Instead, you’re depending on your personal resources, such as pensions, annuities, Social Security, and your savings, to fund your retirement.

This is a psychological shift as well: you are now changing from saving mode to spending mode. So, instead of putting money into your savings accounts, you’re now drawing out of your savings accounts to meet your retirement expenses. This is a tremendous mental transition, one that many people have difficulty making.

What are Retirees’ Main Financial Concerns?

A survey by Schroders, an asset management company, found the majority of retirees (68%) were concerned about running out of money. The main reasons for concern were inflation and higher-than-expected healthcare costs. Another common concern was how best to generate income from their savings.

Running Out of Money

Outliving your money is a huge worry for many retirees. Inflation continues its steady annual climb, healthcare costs keep rising, and people are living longer than ever before. All of that makes retirees worry that they’ll run out of money at some point.

A survey found that nearly two-thirds of retirees feared running out of money. Even those with a retirement plan face concerns: MetLife found that most of its plan sponsors believed more than one-quarter of retirees would run out of funds. On the other hand, according to another survey, almost three-fourths of retirees indicated they have enough money to last through retirement.

Insufficient Income

Another monetary worry is not having enough income to fund an entire retirement. Surveys find retirees are concerned about how best to generate income. Even if they don’t actually run out of money, retirees are concerned their investments may not generate sufficient income to cover their expenses throughout retirement.

Healthcare Costs

Rising healthcare costs are a principal reason people are concerned about running out of money. In 2023, Fidelity estimated a couple would need to spend $315,000 on healthcare in retirement. Estimated healthcare costs have risen each year until 2023 and nearly doubled between 2002 and 2023.

How You Can Address These Concerns

If you’re retired or about to be, and you have financial concerns, the best way to address them is to candidly assess your situation, and then take appropriate action.

Guaranteed Income and Essential Expenses

A good place to start is by considering and comparing your guaranteed income and your essential expenses. Guaranteed income sources include Social Security benefits, pensions, military retired pay, and annuities.

What are Essential Expenses?

Essential expenses are things you have to spend on, such as mortgage payments or rent, loan repayments, groceries, home and car maintenance, and utility bills. These are distinct from nonessential expenses that are not strictly required to live, like gym memberships, cable subscriptions, leisure travel, and daily Starbucks lattes.

When you total your essential expenses, you now know how much you must spend each month in your retirement.

Fixed Expenses Vs. Variable Expenses

Some expenses occur each month and are the same each month, like rent and loan repayments.

Others occur each month but vary from month to month, like groceries and utility bills. For those, take an average of how much you spent each month over the past year.

Still other expenses only occur occasionally, like home and car maintenance. For these occasional expenses, consider how much you spent in the past year and average this amount over 12 months. For example, if you spent $500 on car maintenance in the past year, averaging over 12 months means you spent an average of $41.67 on car maintenance per month.

Your Expenses Are Different in Retirement

Remember that your expenses will be different now that you’re retired. When you retire, some expenses will decrease or go away completely. Many of the expenses that will go away are related to your job, like commuting costs, work-related clothing, professional training and continuing education, and lunches out with coworkers. You may also choose to lower or forego other expenses when you retire, like some types of insurance. If, like most people, your income decreases when you retire, your income taxes will also go down.

If your guaranteed income meets or exceeds your essential expenses, you’re covered. You won’t need to dip much into your savings to meet your living expenses. Therefore, you may consider investing your savings in order to grow your assets for future needs or to pass on to heirs. There’s also free cash left for retirement activities like travel or hobbies.

If your essential expenses exceed your guaranteed income, you’ll need to make up the shortfall from your personal savings. You can use some of your savings to generate cash flow and supplement your guaranteed income.

Create a Budget

The next step is to create a budget. You may have saved and budgeted conscientiously for decades so that you could retire. Now, it’s time to create a retirement budget. You can start with your previous budget and make some changes to reflect your new situation.

If you don’t have a budget, now’s a good time to start one. Budgeting helps you track your income and expenses and ensure your funds will last throughout your entire retirement. It gives you peace of mind that your spending is on track. As mentioned earlier, two-thirds of Americans are worried about running out of money in retirement. A budget can help keep you from being one of them.

Yes, budgeting takes a little time and effort. And it can seem restrictive, like you’re depriving yourself of things you want. But a budget is just that: a projection of your income and expenditures. You’re still in control; your budget just tells you whether you’re on the right track and where you might need to adjust.

How to Create Your Budget

You can create and keep up your budget with a spreadsheet or even pen and paper. If you prefer a higher-tech method, there are many budgeting apps available. Some well-known ones are YNAB (You Need A Budget), EveryDollar, PocketGuard, GoodBudget, and Mint.

The goal of your budget is to identify where every dollar that passes through your hands goes. Every dollar that comes in must be spent, saved, or given away. So, your income minus the total of expenditures, savings, and donations must equal zero. This is called zero-based budgeting.

A benefit of zero-based budgeting is that it shows you exactly what you’re spending money on. You may realize you’ve been paying for a gym membership that you hardly ever use.

It also helps you make conscious choices about your spending. You might decide you want to spend more on entertainment and less on restaurant takeout, for example.

Finally, zero-based budgeting puts saving on an equal footing with spending. For your retirement, which may last for two decades or more, saving is crucial. Your expenses will change after you retire, and you’ll want to plan for the future and future expenses. Yes, even as a retiree, you still need to plan for the future.

Planning for Inflation and Future Expenses

Inflation is a common worry among retirees. Prices are continually rising. Inflation has averaged 3.3% in the U.S. from 1914 to 2024. That means in 20 years, you’ll need $191 to purchase what costs $100 today.

You’ll also need to plan for additional costs down the road. Two of these are healthcare and long-term care. Later in retirement, healthcare costs usually increase. According to a report by RBC Wealth Management, healthcare costs for those aged 65 to 74 are $13,000 per year. For those over the age of 85, those costs rise to $39,000 per year. You might also need long-term care at some point. Long-term care costs may be $100,000 per year or more.

Growing Your Savings

You will need to grow your savings in order to keep pace with inflation and prepare for these potential future costs. A major challenge for retirees is balancing the need for growth with the need for present income. Retirees often rely on bonds, annuities, CDs, and other fixed-income vehicles for present income while investing in stocks for future growth.

You also need to maintain some safety in your investments and avoid taking large losses. High-quality bonds provide a degree of safety and provide income. Stock investments can provide long-term growth, but can also lose value from year to year. So, you need to consider how much to allocate to each, so that you avoid having to sell investments when their value is down.

Financial advisors often suggest the “rule of 100” to determine your allocation: subtract your age from 100 and use that as the percentage to put in stocks. For example, if you’re 65 years old, you would put 35% in stocks and 65% in bonds. If you’re 80 years old, you would put 20% in stocks and 80% in bonds. Your allocation becomes more conservative as you age.

Another way to determine your allocation is to decide how much income you need each month for essential and discretionary expenses, then determine how much you need in bonds, annuities, or CDs to produce that much income. You put any remaining funds in equities.

You might also consider keeping a liquid emergency fund for sudden, unforeseen expenses like home or car repairs or medical bills.

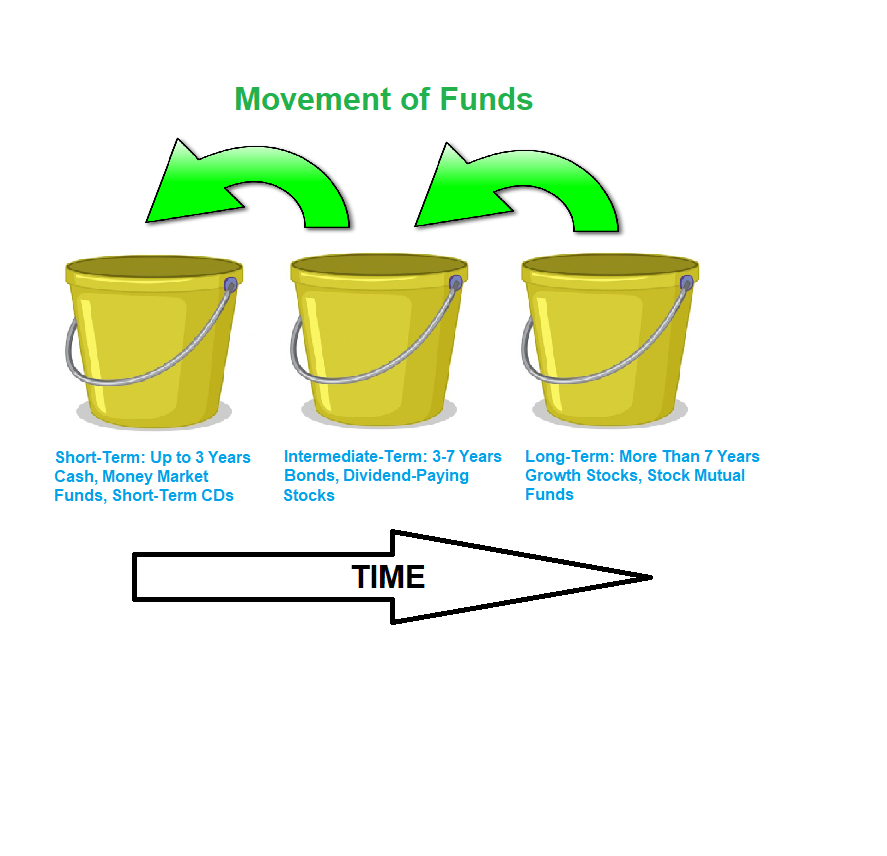

Time Bucket Strategy

A popular strategy for managing finances in retirement is the notion of “time buckets.” You divide your funds into multiple groups, or buckets, based on how soon you will be using the amount in each bucket. Funds in nearer-term buckets are put in more liquid investments like savings accounts, money market funds, and short-term CDs. Intermediate-term funds are put in conservative investments like bonds and stable, dividend-paying stocks. Funds in long-term buckets may be put in growth stocks or stock index mutual funds where they can grow. As you go through your retirement, you move funds between buckets as needed.

The number of buckets and the time horizons are flexible and different for each person’s situation. A common strategy is to have three buckets: the first for funds needed in three years or less, the second for funds you’ll need in three to seven years, and the third for expenses more than seven years out.

As time moves forward, you transfer funds from the later buckets to the earlier ones as you need the money.

This short video explains the three-bucket strategy:

Taxes

Tax planning is a crucial part of your retirement financial plan. It’s important to remember that not all of the funds in your investment or tax-deferred retirement accounts are really yours: you’ll need to pay taxes on withdrawals, interest, and dividends.

Most people’s taxes decrease after retirement because they have lower income. But sound tax planning can help you keep from inadvertently being bumped into a higher tax bracket. You may want to reassess your investments and savings after retirement to preserve the principal and save on taxes. When and how you withdraw funds from your accounts can affect your taxes.

Here are some things to consider:

Stock dividends are usually taxed at lower rates

Qualified stock dividends, which are dividends on publicly traded common stocks, are taxed at capital gains tax rates, which are often lower than ordinary income rates. For capital gains, the tax rate may even be 0%.�

Withdrawals from traditional IRAs are taxed as ordinary income.�Although traditional IRAs and 401(k)s are tax-deferred, your dividends, interest, and capital gains are considered ordinary income for tax purposes.

Many financial advisors suggest taking withdrawals from taxable accounts first, allowing tax-deferred accounts the opportunity to continue growing.

An alternative approach is to take proportional withdrawals: you withdraw from all accounts, both taxable and tax-deferred, based on that account’s percentage of your total savings. For many people, this can lower their overall tax bill and produce higher after-tax income.

Tax-deferred accounts have required minimum distributions.Traditional IRAs and 401(k)s have required minimum distributions (RMDs). Starting from age 73, you must have a certain amount distributed to you. The IRS regards these distributions as ordinary income for tax purposes. Furthermore, the RMD may bump you to a higher income tax bracket.

Medicare premiums are adjusted based on your income.Medicare uses what it calls the Income-Related Monthly Adjustment Amount (IRMAA). Medicate adjusts your premium is based on your income two years prior and recalculates it annually. If withdrawals from your accounts push you into a higher IRMAA bracket, you could suddenly find your Medicare Part B and D premiums have increased.

Tax planning in retirement can be complex and different for each person or couple. You might consider consulting a tax or financial professional for advice regarding your specific situation.

Avoid Scams

Scams are unfortunately a part of life and are becoming more prevalent. One successful scam can derail the best-laid retirement plan. A 77-year-old widow lost $661,000, her entire life savings, to a scam. Scammers often target older adults because many older Americans have substantial savings and tend to be polite and trusting. The emergence of common artificial intelligence tools has enabled scammers to become more sophisticated and convincing in their fraud attempts.

View our financial scams page for more information about protecting yourself from financial scams.

Estate Planning

Estate planning may not be something that a lot of us think about, but it’s an essential part of your retirement financial plan. Many people have the mistaken notion that estate planning is only a concern for ultra-wealthy individuals who are of advanced age. In reality, though, estate planning is for pretty much everyone. It’s a gift you give to your descendants. It’s also the gift of peace of mind you give yourself.

Estate planning is a topic in itself. Feel free to visit our estate planning page for more information.